Friday, March 30, 2012

Mega Millions Number Frequency

Tonight's Mega Millions Lottery is for over $600m, meaning that each ticket has an after tax expected value of almost $2 (assuming no splits). To aid you in finding the best numbers to play tonight, below is a chart of the frequency of each number. The red bars represent the frequency in all drawings, the black squares are the frequency in the last 50 drawings. Good Luck!

Personal Saving Rate

If you're in the camp that one of the major structural problems facing the US economy is that the personal savings rate is too low, then February's personal income data out this morning shouldn't make you feel too optimistic. Just as the stock market is making new highs not seen since 2008, the savings rate is making new lows not seen since a similar time.

Thursday, March 29, 2012

Long Term Capacity Utilization Chart

Given that real GDP has moved beyond its pre-recession high, one might expect that capacity utilization would be narrowing and at least above its own pre-recession mark. However, capacity utilization as reported in February is still only 78.7. Optimists might look at this as a sign that there is still room to improve; pessimists might point to this as being a sign that the economy isn't nearly as strong as sentiment would imply.

Wednesday, March 28, 2012

S&P 200 vs 50 Day Moving Average

Consistent with the laws of mathematics, the 50 day moving average of the S&P 500 is currently above the 200 day moving average. In an attempt to use the divergence of the 50 and 200 dmas as a proxy for how overbought/oversold the index is, below is a chart of the difference between the 50 and 200 dmas since 2008. At the current level, the 50 day is about 100 points above the 200 day. In the last two peaks, this metric got into the 125 area.

Year over Year Change in Monetary Base

Gold's advance has slowed in 2012 compared to recent years, and the metal hasn't traded very well since September of 2011. Still, this morning CNBC is running results from a poll showing that retail investors love the metal. While many professionals will tend to take such a poll as a contrarian indicator, something fundamental may be beginning to change for gold as well. A major driver of gold's advance has been the increase in the monetary base because of QE. If a QE3 doesn't take place then this increase will continue to slow. The increase in the base has already slowed considerably in recent months, as shown below. Of course, gold was strong 2002-2003 despite moderate base money growth, so just because this growth slows doesn't necessarily mean the end for gold.

For The Price of The Dodgers...

A group led by Magic Johnson bought the Dodgers yesterday for $2.15B, the highest amount ever paid for a sports franchise. Below is a list of other assets that could have been bought for $2.15B. The Dodgers do about 10% of the revenue of these publicly traded companies. In addition, the Dodgers revenue has fallen each of the last two years from $282m in 2009.

Tuesday, March 27, 2012

Mega Millions Mega Ball Frequency

A good investor looks for any opportunity in which capital can be deployed into a situation in which a contract can be purchased for $1 that has an expected value greater than $1. With the mega millions jackpot at $356M tonight, this is one of those special times that the expected value of one lottery ticket is actually greater than the dollar it's purchased for (excluding the possibility of a split jackpot). This is because the lump sum after tax value of tonight's jackpot is $191m in the state of California, but the odds of winning are 1:171m. This implies that each ticket is worth roughly $1.12, a statistical arbitrage!

If you live in a mega millions state and are going to try your luck tonight, below is a frequency chart for just the mega ball, showing the all time frequency (in red) and the frequency in the last 50 draws (in blue). In 705 drawings, each number should have been drawn about 15 times. In the last 50, each number should have been drawn about once.

Largest US Companies By Net Income

AAPL may have surpassed XOM as the largest US company in terms of market cap, but as far as net income goes, XOM still is king of the hill. Below is a list of the 20 largest US companies based on Net Income as reported at most recent fiscal year end.

The anomalies, F and AIG were so profitable mainly due to deferred tax benefits. F did do $8B in EBIT last year, but also carries $100B in debt on its balance sheet.

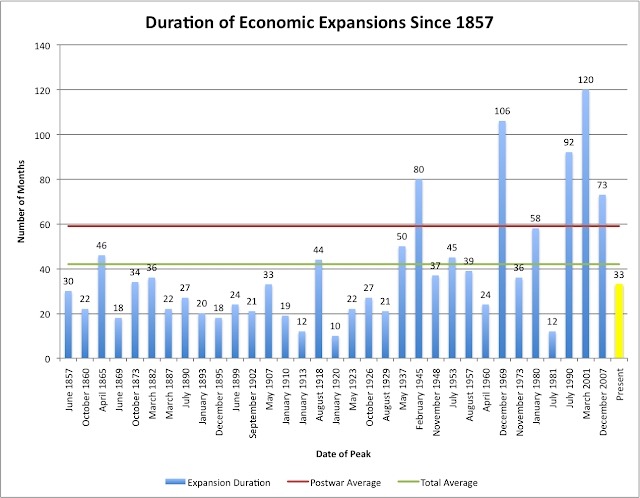

Average Length of Economic Expansion

With the S&P making new cycle highs, and talk of "double dips" a distant memory, we look to previous cycles to guide us as to how long this one could last. Below is a chart of the duration of all economic expansions since 1857.

The current expansion is 33 months old which still puts it below the average of all expansions and well below the post war average. The average expansion since 1857 lasted 42 months; in the postwar era this number jumps to 59 months. Notably, the economic expansion that followed the 1974 bear market (which many argue is the best historical corollary to today's expansion) lasted 58 months, implying that the current expansion could have another 25 months to go. That would put the next recession sometime in 2014.

The current expansion is 33 months old which still puts it below the average of all expansions and well below the post war average. The average expansion since 1857 lasted 42 months; in the postwar era this number jumps to 59 months. Notably, the economic expansion that followed the 1974 bear market (which many argue is the best historical corollary to today's expansion) lasted 58 months, implying that the current expansion could have another 25 months to go. That would put the next recession sometime in 2014.

Monday, March 26, 2012

DFS new leverage targets

Though it probably seemed like it would be a long time before leverage came back to the financial system, the following comment from Discover caught my eye on its most recent conference call. The company is moving from benchmarking equity on a tangible common basis to a Tier 1 (less strict) standard. It is also targeting a lower level of capital and therefore more leverage. From the call:

Turning to capital. For some time now, we have benchmarked our key capital ratio as tangible common equity-to-tangible assets with a target of plus or minus 8%. Going forward, we will switch to focusing on our Tier 1 common capital ratio as it better represents how regulators and the industry look at capital levels, and we have established a 9.5% long-term target. We ended the most recent quarter at 14.3%Apologies to anyone who read this with glaring typos earlier. That's what I get for posting from my iPhone.

Friday, March 23, 2012

Warren Buffett Is Understating The Amount He Pays In Taxes

It's tax season and Friday, so here's my offbeat post for the day:

Last year Warren Buffett wrote a controversial letter to congress claiming that he only paid $6.9m in taxes in 2010 (a 17% tax rate) and suggested that the rich pay more in taxes. Depending on which side of the political spectrum you're on, you might think of Buffett as a hero or as a turncoat, but what you probably didn't notice is that Buffett deliberately understated the amount of taxes that he paid because he didn't include his share of taxes paid through Berkshire Hathaway.

Warren Buffett owns 37.5% of BRK, which earned $15.314B pre tax last year. His share of these pretax earnings was therefore $5.74B. On an accrual basis, BRK paid $4.57B in taxes on these earnings, of which Buffett's share was $1.71B (which is a 30% rate on his share of BRKs pretax profits). In short, Warren Buffett didn't pay just the $6.9m in taxes that he claims, he paid more like $1.72B worth. Only $6.9m was reported on his 1040 though. Buffet pays most of his income tax through his corporate entity.

As the father of modern value investing, Warren Buffett knows better than anyone that an investor's share of the profits earned by a company may as well be personally earned by the shareholder himself. By extension, taxes paid by the company are paid by the shareholder as directly as if they were reported on his personal tax returns. To Buffett, there is little distinction between company and himself. A company is just a legal collective of shareholders, a partnership. In his most recent annual report he touches on this subject in discussing how GAAP does not adequately credit Berkshire for its holdings in WFC, IBM, KO, and AXP because it only allows him to recognize dividends:

Just as Warren Buffett knows that GAAP doesn't account for Berkshire's true economic value derived from owning IBM, WFC, KO and AXP, he also knows that his tax returns don't represent his true income for 2010 and nor does the personal tax liability recognized on his 1040. The $62m that he reported as gross income only represents what he earned as "dividend" from his personal investments. BRK, famously, does not pay a dividend (perhaps so Buffett can avoid paying extra taxes).

Buffett argues to his shareholders that BRK isn't fairly credited for its share of earnings in its "big four" public holdings. But in his letter to congress he ignores his own earnings from his holding of BRK (and by extension the taxes he paid on them). Is it conceivable that Warren Buffett would think of his personal ownership of BRKs earnings differently than BRKs ownership of KO, WFC, IBM and AXP's? If Buffett starts advocating raising the corporate tax rate, then he should start turning heads.

Last year Warren Buffett wrote a controversial letter to congress claiming that he only paid $6.9m in taxes in 2010 (a 17% tax rate) and suggested that the rich pay more in taxes. Depending on which side of the political spectrum you're on, you might think of Buffett as a hero or as a turncoat, but what you probably didn't notice is that Buffett deliberately understated the amount of taxes that he paid because he didn't include his share of taxes paid through Berkshire Hathaway.

Warren Buffett owns 37.5% of BRK, which earned $15.314B pre tax last year. His share of these pretax earnings was therefore $5.74B. On an accrual basis, BRK paid $4.57B in taxes on these earnings, of which Buffett's share was $1.71B (which is a 30% rate on his share of BRKs pretax profits). In short, Warren Buffett didn't pay just the $6.9m in taxes that he claims, he paid more like $1.72B worth. Only $6.9m was reported on his 1040 though. Buffet pays most of his income tax through his corporate entity.

As the father of modern value investing, Warren Buffett knows better than anyone that an investor's share of the profits earned by a company may as well be personally earned by the shareholder himself. By extension, taxes paid by the company are paid by the shareholder as directly as if they were reported on his personal tax returns. To Buffett, there is little distinction between company and himself. A company is just a legal collective of shareholders, a partnership. In his most recent annual report he touches on this subject in discussing how GAAP does not adequately credit Berkshire for its holdings in WFC, IBM, KO, and AXP because it only allows him to recognize dividends:

We view these holdings as partnership interests in wonderful businesses, not as marketable securities to be bought or sold based on their near-term prospects. Our share of their earnings, however, are far from fully reflected in our earnings; only the dividends we receive from these businesses show up in our financial reports. Over time, though, the undistributed earnings of these companies that are attributable to our ownership are of huge importance to us. That’s because they will be used in a variety of ways to increase future earnings and dividends of the investee. They may also be devoted to stock repurchases, which will increase our share of the company’s future earnings.

Just as Warren Buffett knows that GAAP doesn't account for Berkshire's true economic value derived from owning IBM, WFC, KO and AXP, he also knows that his tax returns don't represent his true income for 2010 and nor does the personal tax liability recognized on his 1040. The $62m that he reported as gross income only represents what he earned as "dividend" from his personal investments. BRK, famously, does not pay a dividend (perhaps so Buffett can avoid paying extra taxes).

Buffett argues to his shareholders that BRK isn't fairly credited for its share of earnings in its "big four" public holdings. But in his letter to congress he ignores his own earnings from his holding of BRK (and by extension the taxes he paid on them). Is it conceivable that Warren Buffett would think of his personal ownership of BRKs earnings differently than BRKs ownership of KO, WFC, IBM and AXP's? If Buffett starts advocating raising the corporate tax rate, then he should start turning heads.

Fed Liquidity Swaps

Late last year the Fed reinitiated liquidity swaps with foreign central banks (read: Europe). If memory serves, the move was good for a 3%+ rise in the S&P 500. Now that the crisis in Europe is slowing down for the moment, these swaps have been rolling off the Fed's balance sheet. The swaps did rise slightly last week, but below is a chart showing the progress of the withdrawal.

Thursday, March 22, 2012

Russell 2000 still below 2011 Peak

The S&P 500 and Dow have each by now made new multi year highs. Small caps, however, have not kept pace. The Russell 2000 is still below its 2011 peak, and is underperforming again today.

Dow Recovery From 1929

The good people at Bespokeinvest.com just posted a long term chart of the S&P 500 and Nasdaq which highlighted that while the S&P is only 11% from its all time high, the Nasdaq is still more than 60% away. For historical comparison, below is a chart of the Dow from 1929 through 1958. It shows that it took the Dow almost 25 years to get back to its 1929 peak. After 12 years, the Dow still would need to rise by almost 300% to get back to its peak at 386.

Consecutive Double Digit Quarters

Even after today, the S&P 500 is still up double digits for the first quarter of 2012. This follows another double digit quarter: in 4Q11 the S&P was up 11%. Since 1957, the S&P 500 has only been up double digits two quarters in a row five times. However, if this is the sixth, it would be the third time in three years that it's happened. Below is a list of the times that this has occurred and the performance of the index in the subsequent quarter.

Wednesday, March 21, 2012

Bank Multiples

The XLF is up 21.6% year to date, which is more than any other sector SPDR. KBE, the large cap banking ETF is up a little more than that ~22% driven by BAC which is up a stunning 76% for the year. BAC is still the cheapest large banking stock in the group, trading at just 0.73x tangible book value. Large banks as a whole are still cheaper than their smaller regional counterparts as evidenced by the table below:

Most people would tell you that this discrepancy is driven by concerns over what regulation such as Dodd Frank will do to large banks' earnings power. Will regional banks really earn a 40-50% higher ROE than money center banks will though? That seems to be what the valuations are implying.

Tuesday, March 20, 2012

World Historical Steel Consumption

Along with the previous post, a chart showing total world steel consumption from 1970-2004.

Steel Consumption Statistics

BHP's comments that iron ore demand growth from China will slow helped send the market lower today. In that context, below is China's steel consumption relative to the rest of the world as of 2010.

It may be somewhat surprising to notice that China is far from an emerging market as far as steel is concerned. China is the largest steel producer and consumer in the world on an absolute basis. What's a little more surprising though is that on a per capita basis China consumes much more steel than the US does. Can China grow per capita steel demand even more?

Top Gainers S&P 500 YTD

Presented without much analysis, the top gainers on the S&P 500 year to date. Most of these were significant laggards in 4Q11.

Sunday, March 18, 2012

Best First Quarter for S&P 500

1Q12 is just two weeks from being over and so far it has been quite a quarter. If the quarter closed today, it would be the 9th best 1st quarter since 1957. Below is a list of the other 10 best first quarter performances for the S&P 500.

The list also includes the performance for the the second quarter in those years and for the full year. In 9/10 years the S&P was positive for the rest of the year after a strong first quarter. The second quarter has seen a drop in performance from the first quarter every time though.

It should be noted that the only year that the S&P wasn't positive after the first quarter was 1987, the year of Black Monday. Also, 1998 was the year of long term capital--the index fell back to flat in September, but made all of its ground back in the 4th quarter.

Best 1st Quarters for the S&P 500

Friday, March 16, 2012

Money on the Sidelines

A perpetual bull argument on Wall Street is that "there's so much money on the sidelines" that will continue to push the market higher. For a while in 2009-2011 this was true: individual investors had fled riskier markets and shoved money into lower risk money market funds and CDs. The entire thesis of quantitative easing is that by keeping interest rates low, you can force this money back into riskier assets. As far as this goal is concerned, the two charts below show that the mission has been accomplished.

Retail money market funds made a new multi year low last week. They fell to a level not seen since 1998.

Similarly, small time deposits at US financial institutions are hitting new multi-decade lows. They are about to break through a level not seen since 1980, when this time series (as tracked by the Fed) began.

Retail money market funds made a new multi year low last week. They fell to a level not seen since 1998.

Similarly, small time deposits at US financial institutions are hitting new multi-decade lows. They are about to break through a level not seen since 1980, when this time series (as tracked by the Fed) began.

Federal Budget Sensitivity to Interest Rates

Probably because the S&P is at 1400 and oil is over $100 a barrel, CNBC was legitimately discussing the possibility that the Fed may not be able to keep rates at 0 through 2014. While raising rates would probably be rational in an inflationary environment, below is one reason why the Fed might not be able to raise rates even if they wanted to for the foreseeable future.

The rapid growth in US government debt has made the finances of Uncle Sam extremely sensitive to changes in interest rates. Below is a rough analysis of what the effect of higher interest rates would be on Federal Government interest expense.

If the average rate paid by the US government hit 4% on $15T in debt, then interest expense would be $620B, more than 20% of receipts. At 6% it becomes the largest expense item, more than 35% of receipts. Recall that receipts only represent half of what the government spends, so increases in interest expense are pure increases in deficit.

The rapid growth in US government debt has made the finances of Uncle Sam extremely sensitive to changes in interest rates. Below is a rough analysis of what the effect of higher interest rates would be on Federal Government interest expense.

If the average rate paid by the US government hit 4% on $15T in debt, then interest expense would be $620B, more than 20% of receipts. At 6% it becomes the largest expense item, more than 35% of receipts. Recall that receipts only represent half of what the government spends, so increases in interest expense are pure increases in deficit.

Athlete Pay vs. CEO Pay

There was an article on Bloomberg this morning about the high pay of executives at Berkshire Hathaway. It highlights the following figures:

Berkshire gave $17.4 million in 2011 compensation to Thomas P. Nerney, CEO of its United States Liability Insurance Group; $12.4 million to Geico Corp. CEO Tony Nicely and the National Indemnity Co. unit gave $9.26 million to Ajit Jain, according to filings to state regulators. Berkshire, which is set to send its annual-meeting notice to shareholders today, said in last year’s proxy that Buffett’s salary remains $100,000 at his request.For comparison, here is a list of the highest earning athletes in 2011, broken out by salary and endorsements.

Highest Paid US Athletes

Not a single one of Buffet's execs would have made the top athletes list even though GEICO did $15B in revenue in 2011. The LA Lakers, which paid a $25m salary to Kobe Bryant did about $215m total in revenue. In other words, Thomas Nerney gets paid 2/3 as much as Kobe Bryant to run an organization about 70x larger than the one that Kobe is an employee of.

Nerney obviously isn't the highest paid CEO in America--below is that list based on total comp. Below that is the list if you just included salary. Compare the base salary list to the salary of pro athletes and CEO pay doesn't look so bad.

Thursday, March 15, 2012

High Yield Index Yield

High yield spreads are still slightly wider than they were at this time last year, but since treasury rates have fallen, the effective yield is back to multi-decade (perhaps all time?) lows on the BofA High Yield Master Index. At 14x earnings, the earnings yield of the S&P 500 is roughly the same as the effective yield of the high yield index. Is one of these metrics poised to break lower?

Given that there is a material risk of default for high yield bonds, it would seem that there should be some base level of interest rate received that compensates for the credit risk...if that level is 7.5% then there's not much return to capture from high yield other than carry interest.

Wednesday, March 14, 2012

Treasury Spread vs. CPI

Treasury yields may have finally started to rise over the last several days, but compared to CPI they still haven't risen nearly enough. CPI was up 2.9% y/y as of the most recent reading, but the 10 year treasury bond is only yielding 2.27%. On average over the past 40 years, the 10 year treasury bond has yielded 2.5% (the red line on the chart) more than trailing CPI, which would imply that today's yield should be 5.4%.

|

| Click to Enlarge |

More Stress Test Assumptions

Another important assumption made as part of the stress test:

Some of the AFS/HTM securities are assumed not to be at risk for the kind of credit impairment that results in OTTI charges, including U.S. Treasury and U.S. government agency obligations and U.S. government agency mortgage‐backed securities (MBS)WFC, for example has ~$200B of Treasury, Municipal and Agency obligations. If you assume a 10% loss on these, WFC, often considered to be the strongest large bank in the US, would not have passed the stress test.

Stress Test Assumptions

The Fed released the results of its most recent stress test yesterday, which showed that the majority of US banks have plenty of capital to survive a hypothetical stressed economic scenario. Below are the assumptions that were used to administer the test, which include a 50% decline in equity prices, a 20% decline in housing markets and unemployment increasing to 13%.

The assumptions made for credit spreads are a little bit curious. BBB spreads peak at around 500bps, despite peaking at 800bps in 2008-09, and mortgage spreads also don't increase by much even though the housing market would be falling apart and Fannie and Freddie would likely be in need of another few hundred billion dollars in bailouts.

The assumptions made for credit spreads are a little bit curious. BBB spreads peak at around 500bps, despite peaking at 800bps in 2008-09, and mortgage spreads also don't increase by much even though the housing market would be falling apart and Fannie and Freddie would likely be in need of another few hundred billion dollars in bailouts.

The most egregious assumption is likely the rate on the 10 year treasury though. The most likely reason that the US would enter such a severe recession in the next 5 years is because the government has to balance the budget in a Greek-like austerity. In that scenario treasury yields wouldn't be below 2%.

Tuesday, March 13, 2012

S&P Priced in Gold

The S&P 500 and Gold are curiously divergent for the day of a Fed meeting. One would think that if the Fed signaled more accommodation both might rally, and if more hawkish both might fall. Despite the divergence and gold's underperformance since September, the S&P still hasn't recovered fully from last summer's drop when priced in gold.

Monday, March 12, 2012

Nothing Worth Seeing at the Movies

There's a lot of talk about DIS today after John Carter, which cost $250m to make, flopped by only grossing $30m in its first weekend. Carter continues a rough period for Hollywood in getting audiences to the theaters. In 2011, domestic box office gross was down 3.7% and ticket sales were down 4.2%. While there are a lot of arguments as to why this may be the case, quality has to be a primary one. Not a single movie in the top 10 this week had positive reviews at review aggregator rotten tomatoes. If Hollywood wants people to go to the movies still, they should start making better movies.

How Much Capital Do Fannie and Freddie Need?

They rarely make headlines anymore, but Fannie and Freddie are still under the conservatorship of the US government and both recently filed their 10-k for 2011. As an exercise, I thought it might be interesting to run the numbers on how large the capital deficit is at each institution if they were required to adhere to Basel III requirements. Below are the numbers:

Fannie Mae currently has -$4.5B in equity on its books, and Freddie has a deficit of $146M. This implies that in total the two institutions would need to raise more than $180B in equity in order to be stand alone institutions compliant with Basel III in 2019. This is roughly equivalent to the face value of the Greek Bonds which were just swapped. Any chance that congress deals with this anytime within the next 10 years?

Fannie Mae currently has -$4.5B in equity on its books, and Freddie has a deficit of $146M. This implies that in total the two institutions would need to raise more than $180B in equity in order to be stand alone institutions compliant with Basel III in 2019. This is roughly equivalent to the face value of the Greek Bonds which were just swapped. Any chance that congress deals with this anytime within the next 10 years?

VIX vs. Credit Spreads

The VIX has a 15 handle on it for the first time since last summer. At 15, it's back to an area that it hasn't been able to break through since before the credit crisis. In 2006 though the VIX got into the low teens and bottomed around 10.

Another indicator of financial stress that hasn't been able to reach pre-crisis levels are investment grade credit spreads, which have traded at a structurally higher level since 08 despite seeming to find a bottom/resistance point in the 200 bps area. One thing that's interesting in comparing these two metrics today is that as the VIX has headed lower, credit spreads haven't totally confirmed the move and still remain elevated compared to the last summer.

Another indicator of financial stress that hasn't been able to reach pre-crisis levels are investment grade credit spreads, which have traded at a structurally higher level since 08 despite seeming to find a bottom/resistance point in the 200 bps area. One thing that's interesting in comparing these two metrics today is that as the VIX has headed lower, credit spreads haven't totally confirmed the move and still remain elevated compared to the last summer.

|

| Click to Enlarge |

Thursday, March 8, 2012

Is Facebook Worth $100B?

Facebook will possibly go public with a $100B valuation. Below are some of the important metrics pulled from the S-1 to determine whether that's a reasonable number or not.

Advertising Market Metrics (2010)

Total Advertising Market: $588B

Traditional Ad Spend (TV, Radio, Print): $363B

Online Ad Spend: $68B

Facebook Metrics (2011)

Revenue: $3.7B

Operating Income: $1.75B

Operating Margin: 47%

Analysis:

Online Ad Spend as % of total: 11.5%

Facebook Revenue as % of total online spend: 5.4%

Back of the envelope:

Advertising Market Metrics (2010)

Total Advertising Market: $588B

Traditional Ad Spend (TV, Radio, Print): $363B

Online Ad Spend: $68B

Facebook Metrics (2011)

Revenue: $3.7B

Operating Income: $1.75B

Operating Margin: 47%

Analysis:

Online Ad Spend as % of total: 11.5%

Facebook Revenue as % of total online spend: 5.4%

Back of the envelope:

- If online ad spend grows to 20% of the total ad market in 2015 (above estimates published in the S-1), online spend would be about $120B.

- If Facebook grew its market share of online spend to 9% (currently FB is ~7% of all internet traffic), this would represent about $11B in revenue based on that market size.

- With 47% operating margins, Facebook would earn about $5B in EBIT on that number.

- This means that for $100B Facebook would still trade for 20x operating income (GOOG trades at 17x currently).

- This scenario would imply that Facebook would be flat from its initial valuation, i.e. give 0 return to investors.

- If an investor wanted 10% per year for the next three years from the initial valuation, Facebook would have to be worth $133B in 2015, or 27x operating income--it would also have to grow EBIT at 41% per year for the next 3 years (it grew at 71% in 2011).

Still No Sign of Deleveraging

We're over 4 years into what is supposed to be a once in a generation de-leveraging process. The only problem is that over the past 4 years the entire US non-financial sector (Government, Households and Corporations) has only accumulated more debt on an aggregate basis.

The Fed Flow of Funds report, which came out today, confirmed that debt among these sectors grew by another $1.8T annualized in 4Q11, which is the fastest pace since 4Q08. Households were net accumulators of debt for the first time since 2Q08, paying down $150B (annualized) in mortgage debt but borrowing $170B on credit cards and other consumer credit mechanisms. State and local governments also paid down some debt last quarter as did financial companies, but every other sector accumulated debt.

The Fed Flow of Funds report, which came out today, confirmed that debt among these sectors grew by another $1.8T annualized in 4Q11, which is the fastest pace since 4Q08. Households were net accumulators of debt for the first time since 2Q08, paying down $150B (annualized) in mortgage debt but borrowing $170B on credit cards and other consumer credit mechanisms. State and local governments also paid down some debt last quarter as did financial companies, but every other sector accumulated debt.

|

| Click to Enlarge |

Wednesday, March 7, 2012

Earnings Yield as a Predictor of Future Returns

The chart below is an attempt to measure the extent to which current earnings yield is a predictor of future returns. The blue bars are the earnings yield of the S&P 500 at the recorded date (according to the Shiller P/E, which admittedly may not be the best measure). The red bars are the realized annualized forward returns on the S&P 500 from that date until January 1, 2012. For instance, in 1972 the earnings yield of the S&P 500 was 5.79% and the annualized return between 1972 and 2012 was 6.48%.

There are a couple interesting conclusions from the chart:

1) forward returns do track value to some extent, bulging for those who bought in the 70s and 80s and falling along with earnings yield in the 90s.

2) Past 1990 the two metrics diverge. This is mostly because the time frame over which value is realized is compressed. In other words, whereas a purchase made in the 1960s has had 50 years to smooth returns, a purchase in 2000 has only had 10. It's not surprising therefore that forward returns haven't exactly tracked valuation. However the divergence is extremely informative about what we may expect from the market over the years to come. The fact that the market has performed significantly worse than the "predicted" earnings yield in 2000 implies that the market has risen too slowly since 2000 and is undervalued relative to that date. The fact that it has risen more than the predicted earnings yield in 2008 implies that it has risen too fast relative to that date.

The discrepancy during the 80s shows that the two metrics aren't prefect predictors of each other, but it is food for thought. Also, it should be noted that this analysis did not include returns on the S&P from dividends.

Tuesday, March 6, 2012

March Investor Letter

Below is a letter that is written monthly for the benefit of Avondale Asset Management's clients. It is reproduced here for informational purposes for the readers of this blog.

Opinions voiced in the letter should not be viewed as a recommendation of any specific investment. Past performance is not a guarantee or reliable indicator of future results. Investing is subject to risk including loss of principal. Investors should consider the suitability of any investment strategy within the context of their personal portfolio. For more information on Avondale Asset Management, readers may be directed here.

Dear

Investors,

The

S&P 500 was up another 4% in February and is now up almost 9% for 2012. This return would be wonderful if judged

over an annual timeframe—for a two-month period it is a phenomenal one. Considering that in an average year,

the stock market has historically returned about 8%, 2012 is already outpacing history. In other words, this stellar

performance could continue, but it would be a little out of the ordinary.

As

I mentioned last month, I wasn’t expecting the market to keep the pace it set

in January, but it did. Reflecting

this expectation, our portfolios were modestly out of position last month,

because I raised cash looking for a buying opportunity that never came. Luckily we did have the luxury of a

good January, so we didn’t give up too much ground even though we were

underinvested. For now our

portfolios remain with large amounts of cash waiting for a more appropriate

entry point. Towards the end of

the month there were some signals that the rally was starting to lose momentum

and so I remain comfortable with our levels of cash. As I write this letter the Dow is down nearly 200 points so

maybe the opportunity is finally here.

Though

unexpected, it’s not at all surprising that the market has climbed further than

we planned for. Rallies have a

tendency to persist longer than most expect. Still, markets will eventually correct as valuations become

stretched, and I think this is beginning to occur today. At the October lows, the S&P was

selling with approximately a 10% earnings yield. Today that same yield is about 7.5%. While this level is still favorable

compared to treasury yields, it is less favorable on an absolute basis especially

given rising inflation (I filled my gas tank with $4.77 gas last week). In my opinion investors need more than a

7.5% return to be adequately compensated for the risk of owning equities in

such an environment. At best, 7.5%

is a fair price.

February’s

market has complicated the picture slightly for March. February is often a weak seasonal

period for stocks, but March tends to be a strong one. Because of this, my bias would typically

be to invest heavily in March, but because we rallied in February, purchases in

March would rely on the market going from overbought to even more overbought. Such a scenario is not totally

unthinkable, but stocks never go up in a straight line, and so a March rise

would bring the market to even more dizzying heights. This would likely put markets in a position for a double-digit

drop in the months that follow.

On

a longer time horizon, not much changed in February. On a cyclical basis (1-3 yr ahead), the market seems to be signaling

that 2012 (the fourth year of an economic expansion) will look a lot like 2006

(the fourth year of another economic expansion) when the market returned

13.6%. On a secular (5-10 yr ahead)

basis though there are still lots of obstacles to a healthy economic

landscape. The European Central

Bank continues to add liquidity to the Eurozone, but European economies are

noticeably slowing. In Asia, there

are drumbeats of a European style debt crisis for Japan beginning to sound in

the distance. Meanwhile, the US

continues to run a deficit that is 8% of GDP with a congress that seems

incapable and unwilling to help. At

some point the markets will have to grapple with these issues. The question is when.

Scott Krisiloff, CFA

Opinions voiced in the letter should not be viewed as a recommendation of any specific investment. Past performance is not a guarantee or reliable indicator of future results. Investing is subject to risk including loss of principal. Investors should consider the suitability of any investment strategy within the context of their personal portfolio. For more information on Avondale Asset Management, readers may be directed here.

Monday, March 5, 2012

BP Settlement

BP settled claims with Gulf residents over the 2010 oil spill for $7.8B this weekend. The WSJ is reporting that this settlement plus others yet to come with the justice department puts the final cost to BP likely somewhere in the $40B range.

Compare this result to the initial loss in market cap to BP in 2010. The company went from a $178B company to a $90B company at the height of the selloff. This implies that some were estimating that the cost to BP could be $90B, more than twice what it will likely end up being.

Compare this result to the initial loss in market cap to BP in 2010. The company went from a $178B company to a $90B company at the height of the selloff. This implies that some were estimating that the cost to BP could be $90B, more than twice what it will likely end up being.

Friday, March 2, 2012

Apple is a Luxury Brand

The people over at Bundle.com have apparently done a survey of 700,000 Mac and PC users to cross reference what the computer that one uses says about where he or she shops for clothes. The results weren't particularly surprising: Mac users tend to shop at higher end, more trendy stores. This isn't surprising because Mac users also pay almost double for a computer/phone/tablet that does basically the same thing as a Windows or Android computer/phone/tablet (I happen to be a Mac user).

The survey highlights the extent to which the consumer electronics market has matured beyond competition based on functionality. In an increasingly commoditized consumer electronics world, the gadget that you use says as much about you as the clothes that you wear. Even though a t-shirt from Saks is functionally the same as a t-shirt from Old Navy, one store can price the shirt multiple times higher than the other based primarily on branding. Said differently, Apple is nothing more than a luxury brand.

Subscribe to:

Posts (Atom)